The IRS recently released the 2021 inflation-adjusted amounts for Health Savings Accounts (HSAs).

HSA basics

An HSA is a trust created or organized exclusively for the purpose of paying the “qualified medical expenses” of an “account beneficiary.” An HSA can only be established for the benefit of an “eligible individual” who is covered under a “high deductible health plan.” In addition, a participant can’t be enrolled in Medicare or have other health coverage (exceptions include dental, vision, long-term care, accident and specific disease insurance).

In general, a high deductible health plan (HDHP) is a plan that has an annual deductible that isn’t less than $1,000 for self-only coverage and $2,000 for family coverage. In addition, the sum of the annual deductible and other annual out-of-pocket expenses required to be paid under the plan for covered benefits (but not for premiums) cannot exceed $5,000 for self-only coverage, and $10,000 for family coverage.

Within specified dollar limits, an above-the-line tax deduction is allowed for an individual’s contribution to an HSA. This annual contribution limitation and the annual deductible and out-of-pocket expenses under the tax code are adjusted annually for inflation.

Inflation adjustments for 2021 contributions

In Revenue Procedure 2020-32, the IRS released the 2021 inflation-adjusted figures for contributions to HSAs, which are as follows:

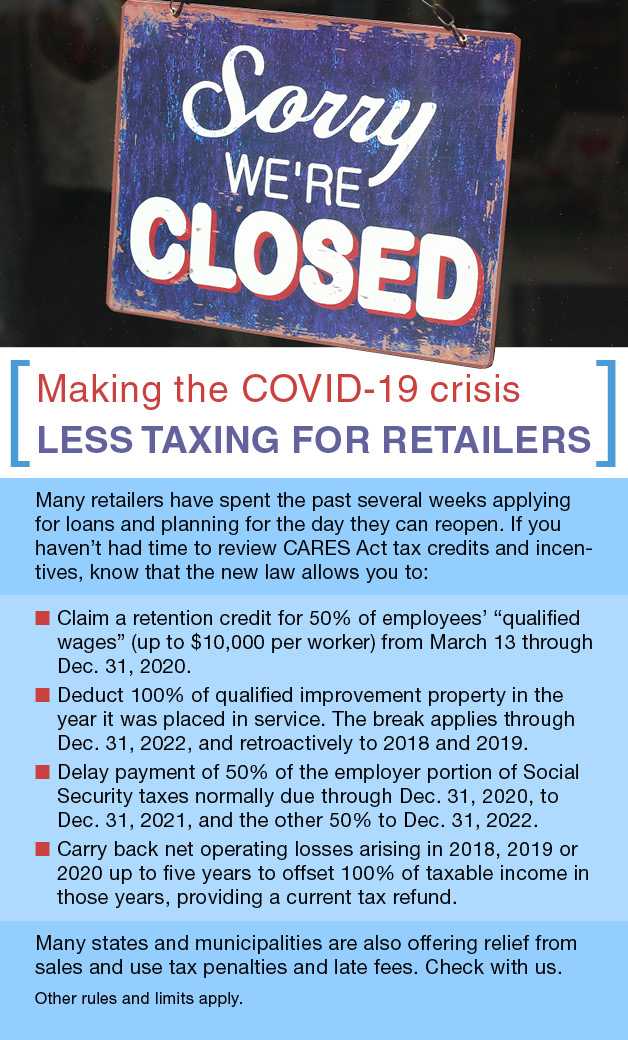

Annual contribution limitation. For calendar year 2021, the annual contribution limitation for an individual with self-only coverage under a HDHP is $3,600. For an individual with family coverage, the amount is $7,200. This is up from $3,550 and $7,100, respectively, for 2020.

High deductible health plan defined. For calendar year 2021, an HDHP is a health plan with an annual deductible that isn’t less than $1,400 for self-only coverage or $2,800 for family coverage (these amounts are unchanged from 2020). In addition, annual out-of-pocket expenses (deductibles, co-payments, and other amounts, but not premiums) can’t exceed $7,000 for self-only coverage or $14,000 for family coverage (up from $6,900 and $13,800, respectively, for 2020).

A variety of benefits

There are many advantages to HSAs. Contributions to the accounts are made on a pre-tax basis. The money can accumulate year after year tax free and be withdrawn tax free to pay for a variety of medical expenses such as doctor visits, prescriptions, chiropractic care and premiums for long-term-care insurance. In addition, an HSA is “portable.” It stays with an account holder if he or she changes employers or leaves the work force. For more information about HSAs, contact your employee benefits and tax advisor.

The IRS has issued guidance clarifying that certain deductions aren’t allowed if a business has received a Paycheck Protection Program (PPP) loan. Specifically, an expense isn’t deductible if both:

- The payment of the expense results in forgiveness of a loan made under the PPP, and

- The income associated with the forgiveness is excluded from gross income under the Coronavirus Aid, Relief, and Economic Security (CARES) Act.

PPP basics

The CARES Act allows a recipient of a PPP loan to use the proceeds to pay payroll costs, certain employee healthcare benefits, mortgage interest, rent, utilities and interest on other existing debt obligations.

A recipient of a covered loan can receive forgiveness of the loan in an amount equal to the sum of payments made for the following expenses during the 8-week “covered period” beginning on the loan’s origination date: 1) payroll costs, 2) interest on any covered mortgage obligation, 3) payment on any covered rent, and 4) covered utility payments.

The law provides that any forgiven loan amount “shall be excluded from gross income.”

Deductible expenses

So the question arises: If you pay for the above expenses with PPP funds, can you then deduct the expenses on your tax return?

The tax code generally provides for a deduction for all ordinary and necessary expenses paid or incurred during the taxable year in carrying on a trade or business. Covered rent obligations, covered utility payments, and payroll costs consisting of wages and benefits paid to employees comprise typical trade or business expenses for which a deduction generally is appropriate. The tax code also provides a deduction for certain interest paid or accrued during the taxable year on indebtedness, including interest paid or incurred on a mortgage obligation of a trade or business.

No double tax benefit

In IRS Notice 2020-32, the IRS clarifies that no deduction is allowed for an expense that is otherwise deductible if payment of the expense results in forgiveness of a covered loan pursuant to the CARES Act and the income associated with the forgiveness is excluded from gross income under the law. The Notice states that “this treatment prevents a double tax benefit.”

More possibly to come

Two members of Congress say they’re opposed to the IRS stand on this issue. Senate Finance Committee Chair Chuck Grassley (R-IA) and his counterpart in the House, Ways and Means Committee Chair Richard E. Neal (D-MA), oppose the tax treatment. Neal said it doesn’t follow congressional intent and that he’ll seek legislation to make certain expenses deductible. Stay tuned.

In light of the novel coronavirus (COVID-19) pandemic, many businesses are interested in donating to charity. In order to incentivize charitable giving, the Coronavirus Aid, Relief and Economic Security (CARES) Act made some liberalizations to the rules governing charitable deductions. Here are two changes that affect businesses:

The limit on charitable deductions for corporations has increased. Before the CARES Act, the total charitable deduction that a corporation could generally claim for the year couldn’t exceed 10% of corporate taxable income (as determined with several modifications for these purposes). Contributions in excess of the 10% limit are carried forward and may be used during the next five years (subject to the 10%-of-taxable-income limitation each year).

What changed? Under the CARES Act, the limitation on charitable deductions for corporations (generally 10% of modified taxable income) doesn’t apply to qualifying contributions made in 2020. Instead, a corporation’s qualifying contributions, reduced by other contributions, can be as much as 25% of taxable income (modified). No connection between the contributions and COVID-19 activities is required.

The deduction limit on food inventory has increased. At a time when many people are unemployed, your business may want to contribute food inventory to qualified charities. In general, a business is entitled to a charitable tax deduction for making a qualified contribution of “apparently wholesome food” to an organization that uses it for the care of the ill, the needy or infants.

“Apparently wholesome food” is defined as food intended for human consumption that meets all quality and labeling standards imposed by federal, state, and local laws and regulations, even though it may not be readily marketable due to appearance, age, freshness, grade, size, surplus, or other conditions.

Before the CARES Act, the aggregate amount of such food contributions that could be taken into account for the tax year generally couldn’t exceed 15% of the taxpayer’s aggregate net income for that tax year from all trades or businesses from which the contributions were made. This was computed without regard to the charitable deduction for food inventory contributions.

What changed? Under the CARES Act, for contributions of food inventory made in 2020, the deduction limitation increases from 15% to 25% of taxable income for C corporations. For other business taxpayers, it increases from 15% to 25% of the net aggregate income from all businesses from which the contributions were made.

CARES Act questions

Be aware that in addition to these changes affecting businesses, the CARES Act also made changes to the charitable deduction rules for individuals. Contact us if you have questions about making charitable donations and securing a tax break for them. We can explain the rules and compute the maximum deduction for your generosity.

The Coronavirus Aid, Relief, and Economic Security (CARES) Act eliminates some of the tax-revenue-generating provisions included in a previous tax law. Here’s a look at how the rules for claiming certain tax losses have been modified to provide businesses with relief from the novel coronavirus (COVID-19) crisis.

NOL deductions

Basically, you may be able to benefit by carrying a net operating loss (NOL) into a different year — a year in which you have taxable income — and taking a deduction for it against that year’s income. The CARES Act includes favorable changes to the rules for deducting NOLs. First, it permanently eases the taxable income limitation on deductions.

Under an unfavorable provision included in the Tax Cuts and Jobs Act (TCJA), an NOL arising in a tax year beginning in 2018 and later and carried over to a later tax year couldn’t offset more than 80% of the taxable income for the carryover year (the later tax year), calculated before the NOL deduction. As explained below, under the TCJA, most NOLs arising in tax years ending after 2017 also couldn’t be carried back to earlier years and used to offset taxable income in those earlier years. These unfavorable changes to the NOL deduction rules were permanent — until now.

For tax years beginning before 2021, the CARES Act removes the TCJA taxable income limitation on deductions for prior-year NOLs carried over into those years. So NOL carryovers into tax years beginning before 2021 can be used to fully offset taxable income for those years.

For tax years beginning after 2020, the CARES Act allows NOL deductions equal to the sum of:

- 100% of NOL carryovers from pre-2018 tax years, plus

- The lesser of 100% of NOL carryovers from post-2017 tax years, or 80% of remaining taxable income (if any) after deducting NOL carryovers from pre-2018 tax years.

As you can see, this is a complex rule. But it’s more favorable than what the TCJA allowed and the change is permanent.

Carrybacks allowed for certain losses

Under another unfavorable TCJA provision, NOLs arising in tax years ending after 2017 generally couldn’t be carried back to earlier years and used to offset taxable income in those years. Instead, NOLs arising in tax years ending after 2017 could only be carried forward to later years. But they could be carried forward for an unlimited number of years. (There were exceptions to the general no-carryback rule for losses by farmers and property/casualty insurance companies).

Under the CARES Act, NOLs that arise in tax years beginning in 2018 through 2020 can be carried back for five years.

Important: If it’s beneficial, you can elect to waive the carryback privilege for an NOL and, instead, carry the NOL forward to future tax years. In addition, barring a further tax-law change, the no-carryback rule will come back for NOLs that arise in tax years beginning after 2020.

Past year opportunities

These favorable CARES Act changes may affect prior tax years for which you’ve already filed tax returns. To benefit from the changes, you may need to file an amended tax return. Contact us to learn more.

June 10, 2020

Employees – who work for tips. If you received $20 or more in tips during May, report them to your employer. You can use Form 4070.

June 15, 2020

Employers – Nonpayroll withholding.If the monthly deposit rule applies, deposit the tax for payments in May.

Employers – Social Security, Medicare, and withheld income tax. If the monthly deposit rule applies, deposit the tax for payments in May.