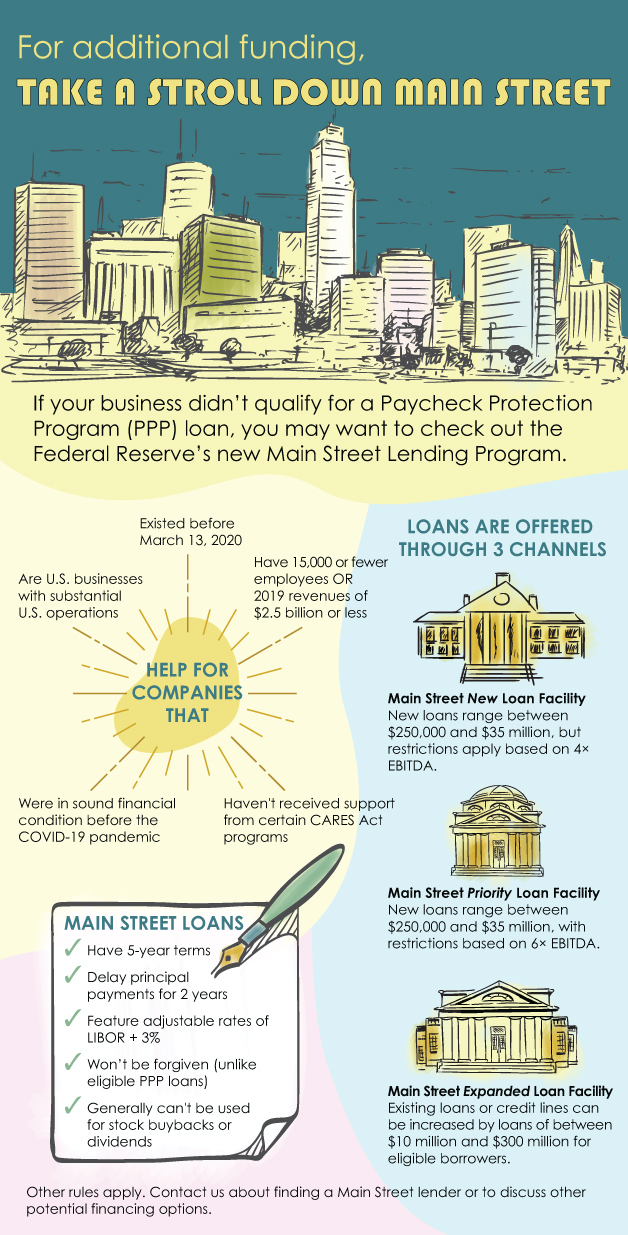

The recent riots around the country have resulted in many storefronts, office buildings and business properties being destroyed. In the case of stores or other businesses with inventory, some of these businesses lost products after looters ransacked their property. Windows were smashed, property was vandalized, and some buildings were burned to the ground. This damage was especially devastating because businesses were reopening after the COVID-19 pandemic eased.

A commercial insurance property policy should generally cover some, or all, of the losses. (You may also have a business interruption policy that covers losses for the time you need to close or limit hours due to rioting and vandalism.) But a business may also be able to claim casualty property loss or theft deductions on its tax return. Here’s how a loss is figured for tax purposes:

Your adjusted basis in the property

MINUS

Any salvage value

MINUS

Any insurance or other reimbursement you receive (or expect to receive).

Losses that qualify

A casualty is the damage, destruction or loss of property resulting from an identifiable event that is sudden, unexpected or unusual. It includes natural disasters, such as hurricanes and earthquakes, and man-made events, such as vandalism and terrorist attacks. It does not include events that are gradual or progressive, such as a drought.

For insurance and tax purposes, it’s important to have proof of losses. You’ll need to provide information including a description, the cost or adjusted basis as well as the fair market value before and after the casualty. It’s a good time to gather documentation of any losses including receipts, photos, videos, sales records and police reports.

Finally, be aware that the tax code imposes limits on casualty loss deductions for personal property that are not imposed on business property. Contact us for more information about your situation.

While the COVID-19 crisis has devastated many existing businesses, the pandemic has also created opportunities for entrepreneurs to launch new businesses. For example, some businesses are being launched online to provide products and services to people staying at home.

Entrepreneurs often don’t know that many expenses incurred by start-ups can’t be currently deducted. You should be aware that the way you handle some of your initial expenses can make a large difference in your tax bill.

How expenses must be handled

If you’re starting or planning a new enterprise, keep these key points in mind:

- Start-up costs include those incurred or paid while creating an active trade or business — or investigating the creation or acquisition of one.

- Under the Internal Revenue Code, taxpayers can elect to deduct up to $5,000 of business start-up and $5,000 of organizational costs in the year the business begins. As you know, $5,000 doesn’t get you very far today! And the $5,000 deduction is reduced dollar-for-dollar by the amount by which your total start-up or organizational costs exceed $50,000. Any remaining costs must be amortized over 180 months on a straight-line basis.

- No deductions or amortization deductions are allowed until the year when “active conduct” of your new business begins. Generally, that means the year when the business has all the pieces in place to begin earning revenue. To determine if a taxpayer meets this test, the IRS and courts generally ask questions such as: Did the taxpayer undertake the activity intending to earn a profit? Was the taxpayer regularly and actively involved? Did the activity actually begin?

Expenses that qualify

In general, start-up expenses include all amounts you spend to:

- Investigate the creation or acquisition of a business,

- Create a business, or

- Engage in a for-profit activity in anticipation of that activity becoming an active business.

To be eligible for the election, an expense also must be one that would be deductible if it were incurred after a business began. One example is money you spend analyzing potential markets for a new product or service.

To qualify as an “organization expense,” the expenditure must be related to creating a corporation or partnership. Some examples of organization expenses are legal and accounting fees for services related to organizing a new business and filing fees paid to the state of incorporation.

Thinking ahead

If you have start-up expenses that you’d like to deduct this year, you need to decide whether to take the elections described above. Recordkeeping is critical. Contact us about your start-up plans. We can help with the tax and other aspects of your new business.

If you operate a small business, or you’re starting a new one, you probably know you need to keep records of your income and expenses. In particular, you should carefully record your expenses in order to claim the full amount of the tax deductions to which you’re entitled. And you want to make sure you can defend the amounts reported on your tax returns if you’re ever audited by the IRS or state tax agencies.

Certain types of expenses, such as automobile, travel, meals and office-at-home expenses, require special attention because they’re subject to special recordkeeping requirements or limitations on deductibility.

It’s interesting to note that there’s not one way to keep business records. In its publication “Starting a Business and Keeping Records,” the IRS states: “Except in a few cases, the law does not require any specific kind of records. You can choose any recordkeeping system suited to your business that clearly shows your income and expenses.”

That being said, many taxpayers don’t make the grade when it comes to recordkeeping. Here are three court cases to illustrate some of the issues.

Case 1: Without records, the IRS can reconstruct your income

If a taxpayer is audited and doesn’t have good records, the IRS can perform a “bank-deposits analysis” to reconstruct income. It assumes that all money deposited in accounts during a given period is taxable income. That’s what happened in the case of the business owner of a coin shop and precious metals business. The owner didn’t agree with the amount of income the IRS attributed to him after it conducted a bank-deposits analysis.

But the U.S. Tax Court noted that if the taxpayer kept adequate records, “he could have avoided the bank-deposits analysis altogether.” Because he didn’t, the court found the bank analysis was appropriate and the owner underreported his business income for the year. (TC Memo 2020-4)

Case 2: Expenses must be business related

In another case, an independent insurance agent’s claims for a variety of business deductions were largely denied. The Tax Court found that he had documentation in the form of cancelled checks and credit card statements that showed expenses were paid. But there was no proof of a business purpose.

For example, he made utility payments for natural gas, electricity, water and sewer, but the records didn’t show whether the services were for his business or his home. (TC Memo 2020-25)

Case number 3: No records could mean no deductions

In this case, married taxpayers were partners in a travel agency and owners of a marketing company. The IRS denied their deductions involving auto expenses, gifts, meals and travel because of insufficient documentation. The couple produced no evidence about the business purpose of gifts they had given. In addition, their credit card statements and other information didn’t detail the time, place, and business relationship for meal expenses or indicate that travel was conducted for business purposes.

“The disallowed deductions in this case are directly attributable to (the taxpayer’s) failure to maintain adequate records,“ the court stated. (TC Memo 2020-7)

We can help

Contact us if you need assistance retaining adequate business records. Taking a meticulous, proactive approach to how you keep records can protect your deductions and help make an audit much less painful.

Restaurants and entertainment venues have been hard hit by the novel coronavirus (COVID-19) pandemic. One of the tax breaks that President Trump has proposed to help them is an increase in the amount that can be deducted for business meals and entertainment.

It’s unclear whether Congress would go along with enhanced business meal and entertainment deductions. But in the meantime, let’s review the current rules.

Before the pandemic hit, many businesses spent money “wining and dining” current or potential customers, vendors and employees. The rules for deducting these expenses changed under the Tax Cuts and Jobs Act (TCJA), but you can still claim some valuable write-offs. And keep in mind that deductions are available for business meal takeout and delivery.

One of the biggest changes is that you can no longer deduct most business-related entertainment expenses. Beginning in 2018, the TCJA disallows deductions for entertainment expenses, including those for sports events, theater productions, golf outings and fishing trips.

50% meal deductions

Currently, you can deduct 50% of the cost of food and beverages for meals conducted with business associates. However, you need to follow three basic rules in order to prove that your expenses are business related:

- The expenses must be “ordinary and necessary” in carrying on your business. This means your food and beverage costs are customary and appropriate. They shouldn’t be lavish or extravagant.

- The expenses must be directly related or associated with your business. This means that you expect to receive a concrete business benefit from them. The principal purpose for the meal must be business. You can’t go out with a group of friends for the evening, discuss business with one of them for a few minutes, and then write off the check.

- You must be able to substantiate the expenses. There are requirements for proving that meal and beverage expenses qualify for a deduction. You must be able to establish the amount spent, the date and place where the meals took place, the business purpose and the business relationship of the people involved.

It’s a good idea to set up detailed recordkeeping procedures to keep track of business meal costs. That way, you can prove them and the business connection in the event of an IRS audit.

Other considerations

What if you spend money on food and beverages at an entertainment event? The IRS has clarified that taxpayers can still deduct 50% of food and drink expenses incurred at entertainment events, but only if business was conducted during the event or shortly before or after. The food-and-drink expenses should also be “stated separately from the cost of the entertainment on one or more bills, invoices or receipts,” according to the guidance.

Another related tax law change involves meals provided to employees on the business premises. Before the TCJA, these meals provided to an employee for the convenience of the employer were 100% deductible by the employer. Beginning in 2018, meals provided for the convenience of an employer in an on-premises cafeteria or elsewhere on the business property are only 50% deductible. After 2025, these meals won’t be deductible at all.

Plan ahead

As you can see, the treatment of meal and entertainment expenses became more complicated after the TCJA. It’s possible the deductions could increase substantially under a new stimulus law, if Congress passes one. We’ll keep you updated. In the meantime, we can answer any questions you may have concerning business meal and entertainment deductions.

July 2020 Tax Deadlines!

July 10, 2020

Employees – who work for tips. If you received $20 or more in tips during June, report them to your employer. You can use Form 4070.

July 15, 2020

Employers – Social Security, Medicare, and withheld income tax. If the monthly deposit rule applies, deposit the tax for payments in June.

Individuals – File an income tax return for 2019 (Form 1040 or Form 1040-SR) and pay any tax due. If you want an automatic 3-month extension of time to file the return, file Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return and pay what you estimate you owe in tax to avoid penalties and interest. Then file Form 1040 or Form 1040-SR by October 15.

Household Employers – If you paid cash wages of $2,100 or more in 2019 to a household employee, file Schedule H (Form 1040 or Form 1040-SR) with your income tax return and report any employment taxes. Report any federal unemployment (FUTA) tax on Schedule H (Form 1040 or Form 1040-SR) if you paid total cash wages of $1,000 or more in any calendar quarter of 2018 or 2019 to household employees.

Individuals – If you are a U.S. citizen or resident alien living and working (or on military duty) outside the United States and Puerto Rico, file Form 1040 or Form 1040-SR and pay any tax, interest, and penalties due. If you want additional time to file your return, file Form 4868 to obtain 3 additional months to file. Then file Form 1040 or Form 1040-SR by October 15.

However, if you are a participant in a combat zone you may be able to further extend the filing deadline.

Individuals – If you are not paying your 2020 income tax through withholding (or will not pay in enough tax during the year that way), pay the first installment of your 2020 estimated tax. Use Form 1040-ES.

Individuals – Make a payment of your 2020 estimated tax if you are not paying your income tax for the year through withholding (or will not pay in enough tax that way). Use Form 1040-ES. This is the second installment date for estimated tax in 2020.

Corporations – File a 2019 calendar year income tax return (Form 1120) and pay any tax due. If you want an automatic 3-month extension of time to file the return, file Form 7004 and deposit what you estimate you owe in taxes.

Corporations – Deposit the first installment of estimated income tax for 2020. A worksheet, Form 1120-W, is available to help you estimate your tax for the year.

Corporations – Deposit the second installment of estimated income tax for 2020. A worksheet, Form 1120-W, is available to help you estimate your tax for the year.

Employers – Nonpayroll withholding. If the monthly deposit rule applies, deposit the tax for payments in June.

July 31, 2020

Employers – Federal unemployment tax. Deposit the tax owed through June if more than $500.

Employers – If you maintain an employee benefit plan, such as a pension, profit sharing, or stock bonus plan, file Form 5500 or 5500-EZ for calendar year 2019. If you use a fiscal year as your plan year, file the form by the last day of the seventh month after the plan year ends.

Certain Small Employers – Deposit any undeposited tax if your tax liability is $2,500 or more for 2020 but less than $2,500 for the second quarter.

Employers – Social Security, Medicare, and withheld income tax. File Form 941 for the second quarter of 2020. Deposit any undeposited tax. (If your tax liability is less than $2,500, you can pay it in full with a timely filed return.) If you deposited the tax for the quarter in full and on time, you have until August 10 to file the return.