October 1, 2023by admin

Here are some of the key tax-related deadlines affecting businesses and other employers during the fourth quarter of 2023. Keep in mind that this list isn’t all-inclusive, so there may be additional deadlines that apply to you. Contact us to ensure you’re meeting all applicable deadlines and to learn more about the filing requirements.

Note: Certain tax-filing and tax-payment deadlines may be postponed for taxpayers who reside in or have businesses in federally declared disaster areas.

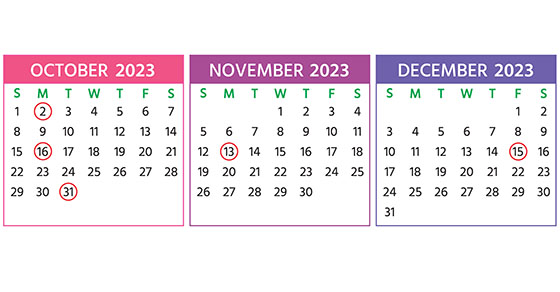

Monday, October 2

- The last day you can initially set up a SIMPLE IRA plan, provided you (or any predecessor employer) didn’t previously maintain a SIMPLE IRA plan. If you’re a new employer that comes into existence after October 1 of the year, you can establish a SIMPLE IRA plan as soon as administratively feasible after your business comes into existence.

Monday, October 16

- If a calendar-year C corporation that filed an automatic six-month extension:

- File a 2022 income tax return (Form 1120) and pay any tax, interest and penalties due.

- Make contributions for 2022 to certain employer-sponsored retirement plans.

- Establish and contribute to a SEP for 2022, if an automatic six-month extension was filed.

Tuesday, October 31

- Report income tax withholding and FICA taxes for third quarter 2023 (Form 941) and pay any tax due. (See exception below under “November 13.”)

Monday, November 13

- Report income tax withholding and FICA taxes for third quarter 2023 (Form 941), if you deposited on time (and in full) all of the associated taxes due.

Friday, December 15

- If a calendar-year C corporation, pay the fourth installment of 2023 estimated income taxes.

Contact us if you’d like more information about the filing requirements and to ensure you’re meeting all applicable deadlines.